ESCT Rate – Set and forget on 1 April

Setting the ESCT rate for the next tax year is a 1 April activity that Payroll are responsible for. As part of your payroll checks and balances, you must check your payroll system is doing as expected. If you are processing payroll manually, you will need to set the ESCT yourself. Understanding how ESCT is essential to getting this right for anyone involved in payroll.

What is ESCT?

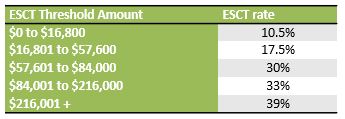

ESCT (Employer Superannuation Contribution Tax) is a tax which is deducted from employer contributions to employees’ KiwiSaver or other complying funds. The correct rate of ESCT to apply to each employee is based on the employee’s marginal tax rate. However, determining which rate will apply requires knowledge of an employee’s annual income.

The ESCT rate is calculated based on the employee’s ESCT threshold. This is the total of the employee’s gross salary or wages, plus any superannuation contribution paid by the employer only (not anyone else they have worked for) to KiwiSaver or any other superannuation fund in the previous tax year (1 April to 31 March).

This gets reset every year on 1 April based on the previous year. If the employee was not employed by the organisation for all of the previous tax year, the ESCT Threshold is estimated based on the total amount of salary or wages plus gross employer contributions that the employee will earn in the year ahead.

ESCT is not applied in the same tiered way as personal income tax rates and only one rate applies to the total amount of the employer contribution. ESCT is applied at a flat rate based on the most appropriate rate for each employee. That ESCT rate is based on the ESCT Rate Threshold Amount, which is determined based on historical data or predicted information, depending on the length of service of a particular employee.

When Employee first starts work

The ESCT rate is calculated by making a “reasonable estimate” of what the employee’s relevant remuneration will be from the day they started to the next 31 March.

At 1 April If the employee has not worked for the employer for the full tax year

The ESCT rate is calculated by making a ‘reasonable estimate’ of what the employee’s relevant remuneration will be for the coming year.

If the employee has worked for a full tax year

The ESCT rate is calculated based on the actual relevant remuneration for the previous year to 31 March.

Once it has been set, leave it alone!

ESCT is a final tax and only gets changed at start of employment, or on April 1st, no matter what happens during the year. If an employee has a pay rise during the year, the ESCT does NOT change until 1 April following year.

As we all know, software does not always do things correctly, so always check your ESCT rates on 1st April each year.

This is one of the many topics covered in the Payroll Essentials Training Course. Click here for more information, or fill in the details below.